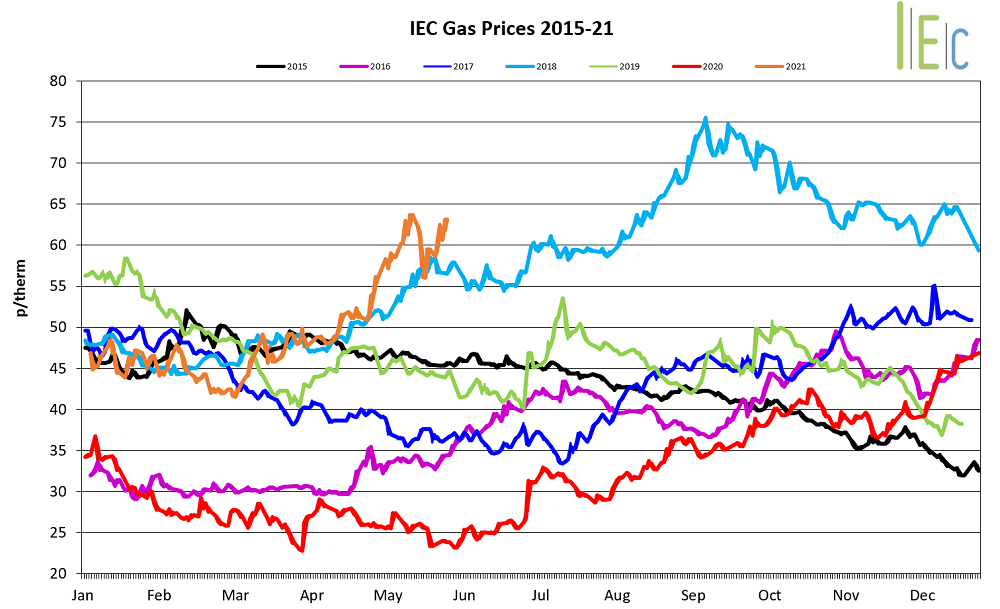

Across May, Gas prices have continued to follow the increasing trend seen in March & April. The increases have been due to several reasons including below-average temperatures since the start of the year causing increased consumption and lower than expected renewable generation and supply issues caused by both planned and unplanned maintenance across Europe. Both of these factors have also prevented gas storage from being replenished during the spring and are only at approx. 30-45% capacity, adding further nervousness to the market. The bullishness of the wider commodity markets, in particular Carbon, have also helped in supporting prices.

However, despite the increasing trend, there was a brief dip in the middle of the month caused by the completion of several planned maintenances and a short-lived drop in the European carbon markets.

The one-year-forward price has, therefore, risen since last month, closing at 63.11ppt on 27th May in comparison to 56.14ppt on 30th April.

Power

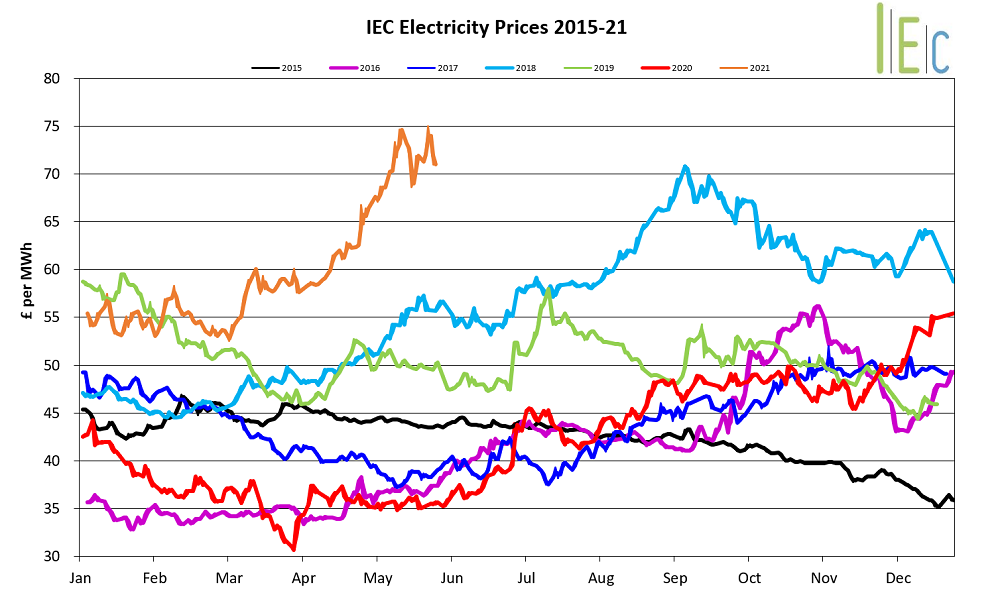

Consistent with the gas markets, overall commercial power prices have continued to rise throughout May, though its journey has been more of a ‘mixed bag’. The main causes behind the increases were due to below-average temperatures which are supporting wider commodity markets. The low wind has significantly limited the percentage of renewables in the power generation mix, and strong carbon pricing in both Europe and the new post-Brexit created UK Emissions Trading Scheme which had its first auction mid-May.

A mid-month dip occurred after significantly improved weather forecasts were given for the end of the month and into June, a short period of high wind boosting renewable generation, coupled with a brief fall in the EU carbon markets – there was an edginess in whether the first auction of UK ETSs would close well below European prices, as the minimum price had been set at £22/tonne. However, market fears were allayed after prices reached over £50/tonne.

The month ended bearishly due to the increased likelihood of the forecasted warmer weather for June being realised, with the one-year-forward price closing at £70.98/MWh on 27th May.

Oil

Brent Crude continued to weaken at the beginning of May as the concern over the Indian COVID-19 variant continued, US and Iranian crude oil stocks increased, the US removed sanctions on Russia surrounding the Nordstream 2 pipeline, and a strong US Dollar pressured down economies.

However, the successful roll-out of the COVID-19 vaccination in China, the US, and Europe led prices of Brent Crude to increase towards the end of May, with the end of lockdown restrictions predicted to result in increasing demand over the summer months.

Coal

The efforts of the UK government to confine coal power to history progressed during mid-May as, after marathon talks, G7 agreed to crack down on coal power use at home and abroad.

In a recent report, the IEA called for no more investment in new fossil fuel supply projects and no further final investment decisions for new unabated coal plants, claiming this is the only way we will hit our goal of net-zero emissions by 2050.

Processing...

Thank you!Your subscription has been confirmed.You'll hear from us soon.