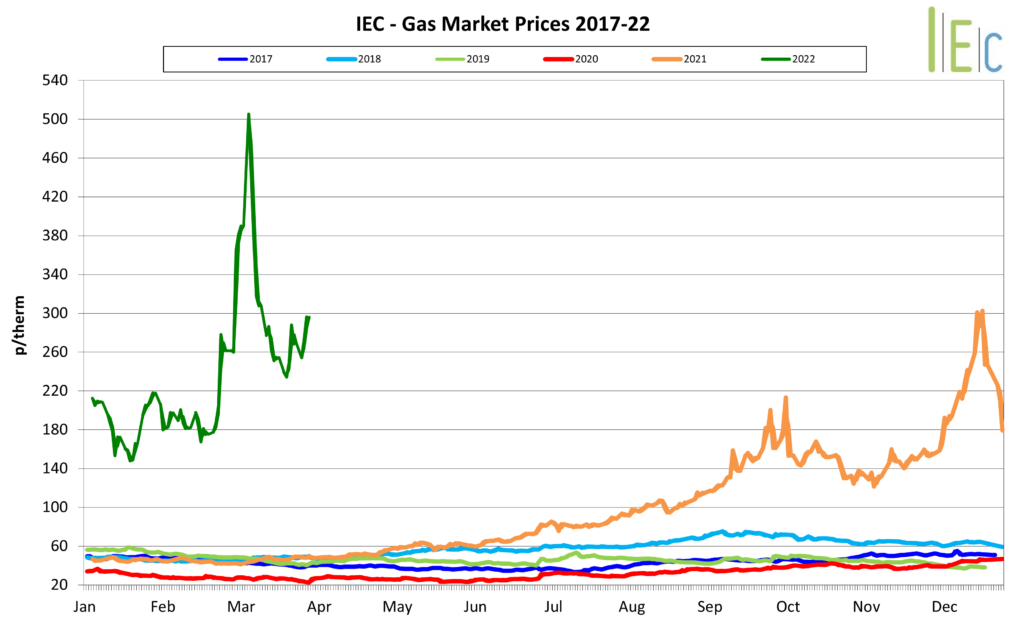

The UK gas market opened in March on an aggressively upward curve, on the back of Russia’s invasion of Ukraine and the potential geopolitical sanctions and supply-chain issues which followed. These fears peaked on 7th March resulting in all-time market record highs. However, with these prices unsustainable, supply chains becoming reassured and additional trade deals agreed, the markets have recovered to around pre-conflict levels.

In line with previous months, the major anxiety in global gas market has been created due to Europe’s potential gas supply issues, through both poor storage levels and future supply. As the early geopolitical sanctions which Europe could apply to punish Russia were being considered, it was the potential that these could include energy exports which intensified market uncertainty. However, the markets began to ease once major EU nations confirmed that essential energy exports would not be included in any sanctions. The price slide continued after Russia omitted energy and raw materials from their own export bans, and EU agreeing alternative supply deals, particularly with the US. However, rumours Russia will demand that their gas exports be paid for in roubles has heightened volatility again, with a series of rebounds in the markets towards the end of month.

Despite the ongoing conflict and ongoing political tensions, Russian gas supply into Europe has not been interrupted. EU Storage levels remain around 10% below the 5-year average.

The UK gas system has continued to enjoy positive fundamentals, with above average temperatures throughout March reducing the domestic heating load. Supply has also been stable, barring an issue at Norway’s Troll field which added anxiety to the markets during the brief rebound mid-month. LNG imports have also been boosted, with around 25 cargoes arriving into UK storage stations. UK gas storage levels site at approx. 77% – significantly above the 5-year average.

Electricity

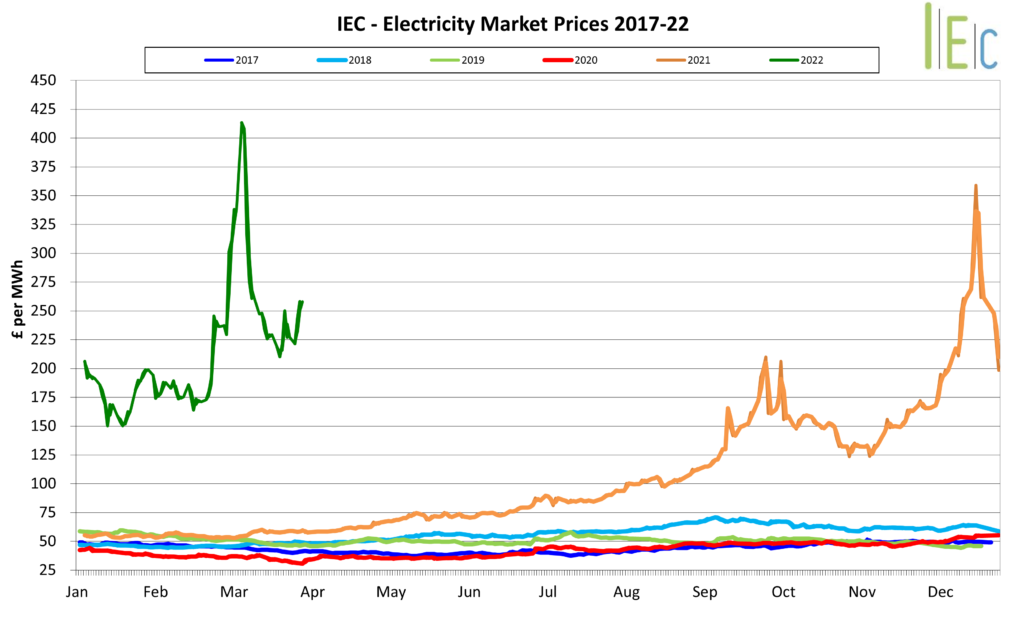

The UK electricity market continues to follow the trends of its gas counterpart, experiencing significant gains in early March before declining again.

Renewable generation has not been as beneficial as in previous months, averaging at between 20-30% of the UK’s power mix. Extra dependence on gas for power generation has been required, strengthening the correlation between both markets.

There were minimal supply issues across March, with additional capacity being imported from the Netherlands.

Both EU and UK carbon markets started the month in with a heavy decline, as the Russia-Ukraine conflict reduced trading confidence and compliance deadlines closing at the end of February. Since then both markets have steadily increased, with prices reaching around the same levels which they started – EU ETS €82 and UK ETS £79 per tonne of carbon.

Processing...

Thank you!Your subscription has been confirmed.You'll hear from us soon.