Gas market trends

What’s been happening?

- In July, day-ahead gas prices increased 4.0% to average 57.7p/th

- Day-ahead gas prices have been driven higher by low levels of wind output, which increased gas demand for power generation, as well as strong demand for storage injection across Europe and low levels of LNG imports. This was despite the gas system being oversupplied for the majority of the month

- The month-ahead (August) gas contract went up 3.8% to average 57.8p/th, peaking at 59.6p/th on 10 July

- All seasonal gas contracts grew in July, up 5.1% on average

- Winter 18 and winter 19 gas averaged 64.2p/th and 59.0p/th, up 2.5% and 5.6% respectively

- Summer 19 and summer 20 gas both went up 6.3% to average 51.4p/th and 46.5p/th respectively

- The annual October 18 gas contract grew 4.2% to 57.8p/th

Key market drivers

- Low wind output amid the ongoing heat wave has led to increased gas for power demand, supporting prices. Strong gas demand for storage injection and high LNG prices have also provided upwards pressure

- Rising EU ETS carbon prices have acted to lower demand for coal-fired generation and consequently lift demand for gas-fired generation

- A 24-hour strike organised by UK workers at Total’s North Sea platforms affected 10% of UK gas production on 23 July. A further strike on 30 July, and planned strikes on 6, 12 and 20 August lifted prices

* £ per p/therm (Annual Forward Average)

Electricity market trends

What’s been happening?

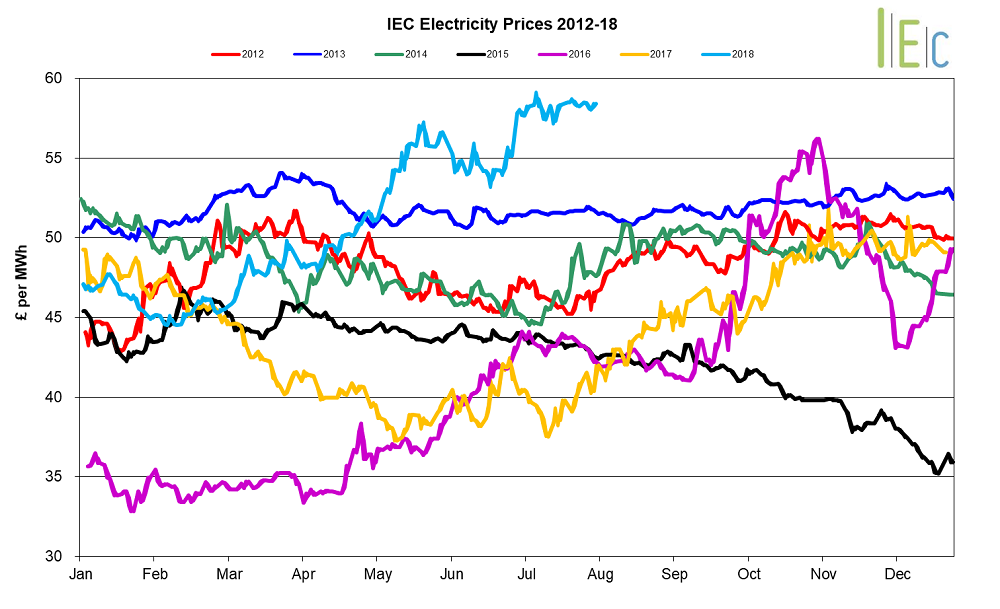

- Day-ahead power grew 6.3% throughout the month to average £57.6/MWh. Day-ahead power peaked at £59.5/MWh on 17 July, a four-month high

- Day-ahead power prices have reflected the fall in renewables generation throughout July and followed gas prices higher

- The month-ahead (August) power contract gained 4.4% to average £56.4/MWh

- All seasonal power contracts rose, gaining 3.7% on average across July. Winter 18 increased 2.9% to £61.9/MWh

- Summer 19 and winter 19 power both rose 4.7% to average £51.0/MWh and £57.0/MWh respectively

- Contracts for summer 20 and winter 20 delivery were up 4.3% and 2.2% to £46.6/MWh and £53.7/MWh

- The annual October 18 power contract increased 3.7% to average £56.5/MWh

Key market drivers

- Average demand increased month-on-month, rising from 0.65TWh to 0.66TWh. Average peak demand also grew month-on-month, rising from 31.4GW in June to 31.8GW in July

- Prices have reflected volatile commodity prices, with gas directly affecting power prices, particularly in periods of lower renewables generation. Higher EU ETS carbon prices have also supported the power curve

* £ per MWh (Annual Forward Average)

European gas

- All tracked European gas contracts climbed in July. British NBP and Belgian Zeebrugge both increased 7% to 58.4p/th and 59.1p/th respectively, whilst German NCG and Dutch TTF both rose 1% to 58.0p/th and 57.7p/th respectively

- July saw an increase in gas for power demand across Europe amid the heatwave, which resulted in more fossil fuel generators being called on as renewables and nuclear output fell. Strong gas demand for storage injection across Europe has also kept prices high

- Prices were also influenced by bullish EU ETS carbon prices, which have made gas-fired power generation more economical relative to coal-fired generation

- Qatari LNG deliveries to Europe have fallen from 107 cargoes in H117, to only 94 in H118. This comes as high demand continues in Asia, which received a higher volume of Qatari deliveries in H118 than in H117. The UK has seen the biggest reduction in supply, which was below 1.0mn mt for H118, down from nearly 2.5mn mt for H117. Asian benchmark price for spot LNG remains higher than the European hub pricing at $10.1/MMBtu and $8.0/MMBtu respectively, a trend which is expected to continue. This has acted to lift European gas prices

- Ongoing geopolitical tensions surrounding the US-China trade war have yet to include LNG, which has continued to remain off any tariff lists. Future additional tariffs could alter the destination of US LNG and see more available for Europe, and provide some downwards pressure to prices

- The gas pipeline between Britain and the Netherlands will be offline for maintenance between 6:00am on 17 September and 6:00am on 20 September according to an announcement by operator BBL on 25 July. The offline maintenance period could constrain supplies and support prices

European power

- European power prices saw bullish movement in July

- Dutch power prices experienced the greatest growth, rising 81% across the month to £35.7/MWh

- French prices rose as extreme temperatures led EDF to reduce nuclear power production at Bugey and Saint-Alban power plants from 28 July. The announcement came after French nuclear power plant output rose in the week commencing 23 July for the first time since May, and a week after EDF’s Bugey-3 reactor saw outages on 21 July due to cooling water restrictions as temperatures rose in the river Rhone

- French prices also rose early in the month following nuclear supply concerns for winter, causing year-ahead power prices to reach one-year highs as issues were discovered at Belgium’s Tihange-3 nuclear power unit

- Power demand in France rose 1.6% on year in July, hitting 34.3TWh amid the ongoing heatwave, with power demand peaking at 58.0GW on 26 July according to data from grid operator RTE

- German power prices spent the month well above seasonal normal levels as wind supplies continued to remain low across Europe, resulting in an increase in fossil fuel generation as renewables output falls

World oil

- Brent crude oil prices fell 0.5% to average $75.2/bl during July.

- Prices were supported early in the month after the announcement of Force Majeures at ports in Libya. Brent crude peaked at $79.1/bl on 9 July, following workers at an oilfield in Norway starting a strike, adding to recent supply disruptions in Libya and Canada. The ongoing geopolitical tensions amid the US-China trade war have led to volatility in the oil market, with some Chinese importers looking elsewhere for supplies, including suggestions of Iranian crude as an option as many other Asian countries look to cancel their Iranian crude imports ahead of US sanctions on the country in November.

Coal

- API 2 coal rose 1.6% to average $89.4/t in July. Prices hit a fresh five-year high of $93.1/t on 10 July. Strong demand in Asia and an increasingly tight supply market has supported prices across the month. Coal tariffs were also highlighted as a potential subject in the US trade war as US President Donald Trump threatened to impose further sanctions. Coal prices declined towards the end of the month, despite an uptick in European demand, notably in Germany amid lower hydro-stocks.

Carbon (EU ETS)

- EU ETS carbon prices gained 7.5% to average €16.4/t, hitting €17.6/t on 24 July – a fresh seven-year high. Carbon prices have been supported by rising power demand across Europe as the power sector responds to increased cooling demand amid the ongoing heatwave. Hydropower reservoirs have also been negatively impacted as they run low, with depleted river levels reducing cooling water availability for nuclear power plants, increasing demand on coal fired generation. Prices are currently above many predictions made by analysts in Q2 18, with most expecting EUAs to reach this high at the end of 2018 ahead of the Market Stability Reserve launch in January 2019.