Gas Market Trends

What’s Been Happening?

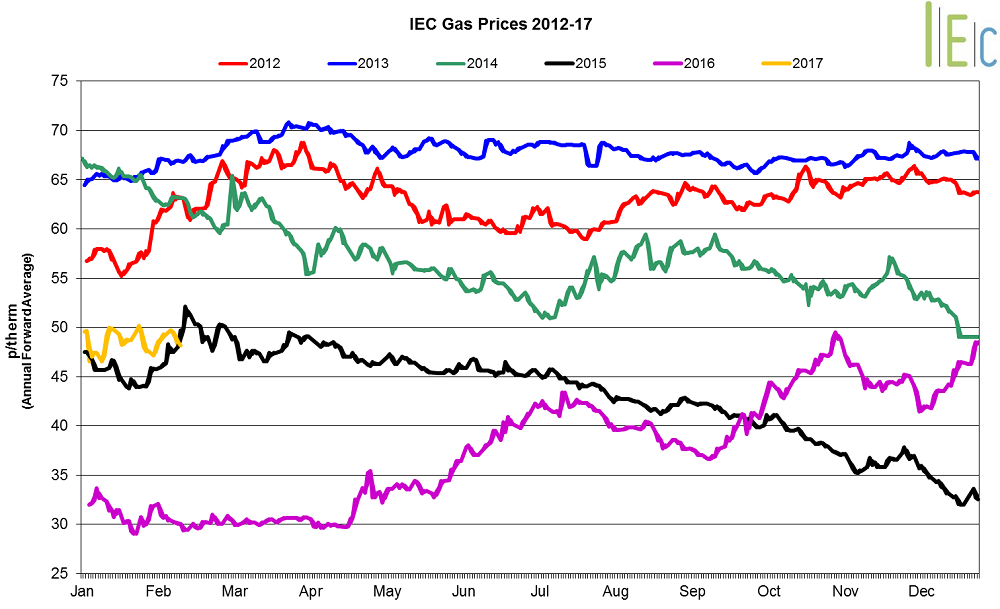

- All seasonal gas prices gained during January, rising 5.3% on average

- Seasonal gas prices remained higher than their levels last year

- Summer 17 gas experienced the largest rise, up 8.4% to average 45.9p/th. Winter 17 gas went up 6.0% to average 51.0p/th

- In January, day-ahead gas jumped 14.7% to average 53.4p/th. On Thursday 12 January, day-ahead gas reached 56.8p/th, the highest price in over two years, with the Met Office issuing national severe weather warnings for snow and wind

- The month-ahead contract moved 13.5% higher to average 53.4p/th

Key Market Drivers

- On 9 December, gas withdrawals from Rough gas storage facility restarted, following restricted operations at the site due to safety checks. Since the restart, capacity reductions have been announced, supporting the near-term contracts. At the end of January, Centrica announced that an outage reducing withdrawals would be extended by a month until 1 March

- Increased oil and coal prices supported gas prices in January

* £ per p/therm (Annual Forward Average)

Electricity Market Trends

What’s Been Happening?

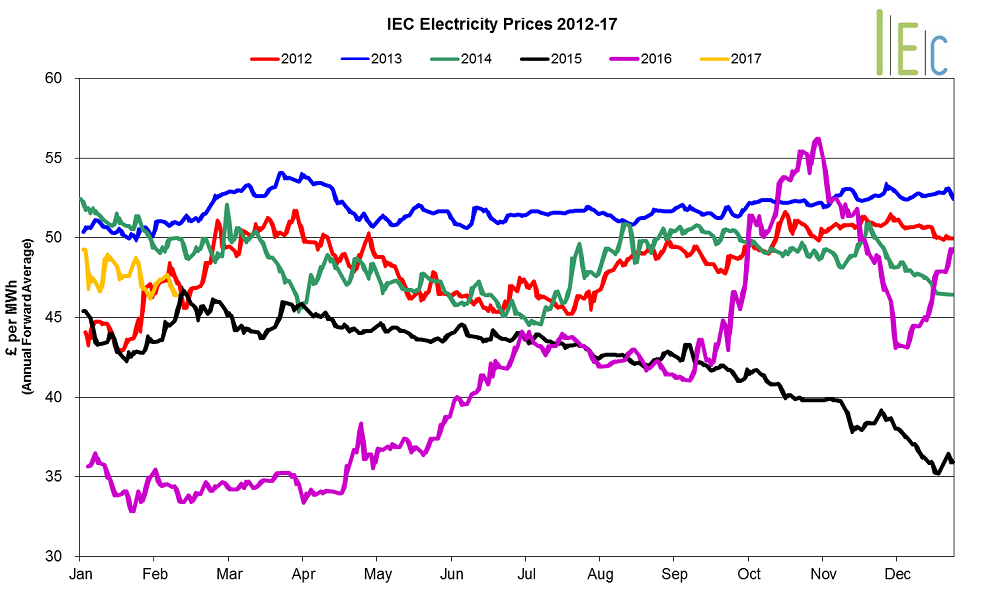

- The annual April 17 baseload power contract climbed 5.1% to average £47.4/MWh

- All seasonal baseload power contracts moved higher, with an average increase of 4.6%

- Summer 17 power was up 6.7% to £45.8/MWh. Winter 17 power rose 3.7% to £49.1/MWh

- Day-ahead baseload power gained by 8.7% to average £53.2/MWh in January, after experiencing losses in December

- The month-ahead contract rose 3.5% to £54.8/MWh

Key Market Drivers

- Low temperatures across northwest Europe and increased energy demand resulted in spikes in electricity prices across the continent

- On 26 January, peak electricity demand on the transmission network reached 51.7GW, which was the highest demand level seen this winter so far

- Increased gas, oil and coal prices supported power prices in January

*£ per MWh (Annual forward average)

European Gas

- European gas prices all increased in January

- GB prices ended the month 1.3% below Belgian prices, 6.2% higher than German prices and 5.0% above Dutch prices

- European gas and power prices were supported by OPEC’s historic agreement from the meeting held on 30 November. At the meeting, OPEC agreed on its first oil output reduction since 2008, in a move to support oil prices

- Data from the Spanish grid operator, Enagas, showed that Spanish gas usage in January rose 24% year-on-year to 38.5TWh, with substantially stronger demand from gas-fired power generation amid weak hydro and wind generation

- Forecasts by the Weather Company show most of Europe is set for warmer-than-normal temperatures during February and March, which could lead to decreased gas demand levels

European Power

- European power prices experienced mixed movements in January

- GB prices ended the month 1.4% above French prices, 20.0% higher than German prices and 21.4% above Dutch prices

- The UK-France power interconnector was damaged on 21 November. National Grid confirmed at the end of November that half of the link’s 2GW capacity will be out of action until the end of February

- Low temperatures across northwest Europe and increased energy demand resulted in spikes in power prices across the continent

- German day-ahead peak load power prices rose on 16 January to its highest level since 2008, with a lack of wind power, combined with nuclear outages during the winter and strong regional demand due to cold weather

- On 24 January, Spanish power prices for day-ahead delivery hit €93.5/MWh, the highest day-ahead price since Platts started assessing it in mid-2007. Prices were lifted by several drivers such as low wind and strong demand

- On 31 January, a total 7.0GW nuclear capacity was lost at 14 French nuclear reactors, following the third strike of the month by EDF workers. Data from the French system operator, RTE, data showed this led to a spike in intra-day prices

- According to RTE, Spain was the country exporting most power to France during the severe drop in temperatures between 16-25 January. France relied heavily on imports to cover the highest demand for electricity in the country since the prolonged cold spell of February 2012

World Oil

- Brent crude oil prices rose 1.4% to average $55.7/bl in January.

- Prices remained above the $50.0/bl mark for the second consecutive month. They remained well above the level in January 2016, when prices averaged $32.1/bl. Prices were heavily influenced by the output cuts of OPEC and non-OPEC members, which came into action at the start of January and are expected to last through until June.

Coal

- API 2 coal prices fluctuated throughout the month, but on average went up 1.2% to $66.7/t. On 18 January prices hit $69.0/t, an eight-week high. Prices rose in January amid concerns that another cold snap in February could boost demand and freeze supply routes. In contrast, the Chinese New Year celebrations (which begin on 28 January and typically last three weeks) could lead to a drop-off in Chinese coal demand moving into February.

Carbon (EU ETS)

- EU ETS carbon prices varied between €4.8/t to €6.3/t, and on average increased 2.0% to €5.3/t. Prices started the month above €6.0/t, but soon dipped and continued to fluctuate through the month.