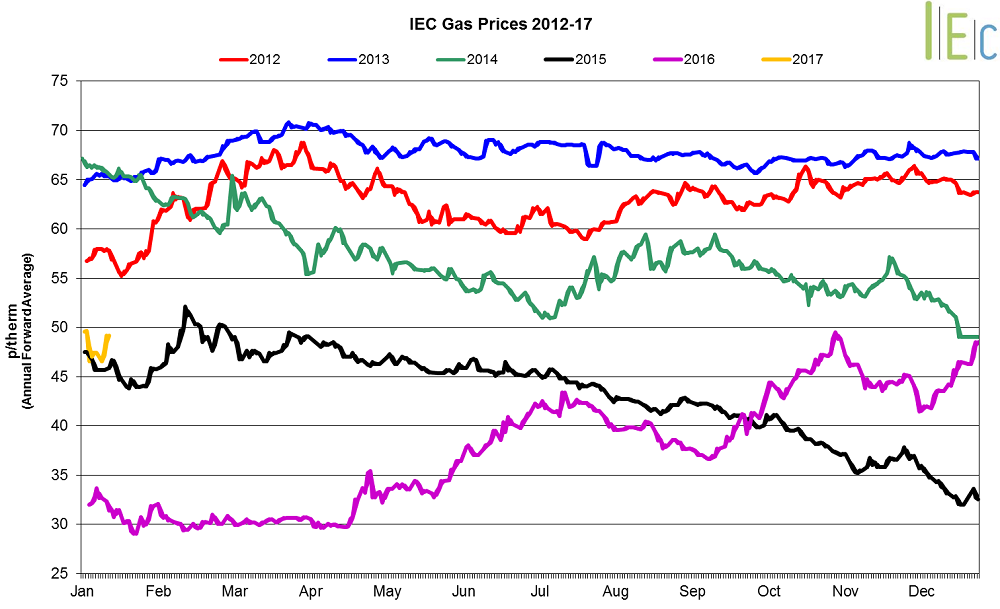

Gas Market Trends

What’s been happening?

- Seasonal gas prices remained relatively unchanged in December, gaining only 0.1% on average

- Winter 17 gas experienced the largest rise, up 0.5% to average 48.1p/th. By contrast, summer 17 gas dropped by 1.0% to average 42.4p/th. Seasonal gas prices remained higher than their levels last year

- In December, day-ahead gas slipped 3.9% to average 46.5p/th. On 8 December, the contract reached a near two-month low, of 41.9p/th

- The month-ahead contract moved 7.7% lower to average 46.8p/th

Key Market Drivers

- On Friday 9 December, gas withdrawals from the Rough gas storage facility restarted, following restricted operations at the site due to safety checks. This led to an easing of prices in near-term contracts. However, since the restart, further maintenance and capacity reductions have been announced, which could support near-term contracts at the start of 2017

* £ per p/therm (Annual Forward Average)

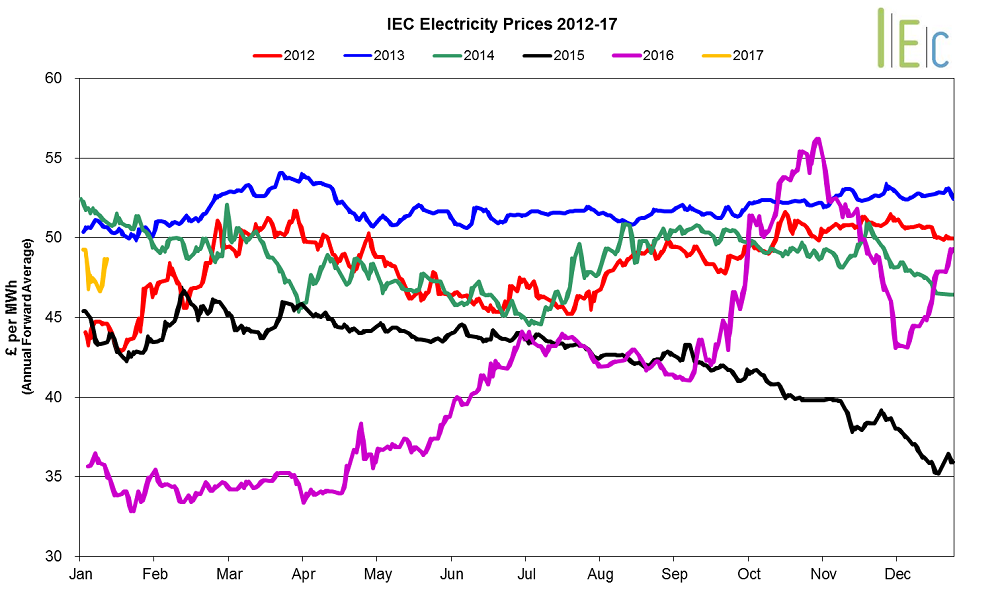

Electricity Market Trends

What’s been happening?

- The annual April 17 baseload power contract slipped 1.9% to average £45.1/MWh

- Seasonal baseload power contracts also remained relatively stable, with an average decrease of 0.1%

- Summer 17 power experienced the largest fall of 2.2% to average £42.9/MWh

- Day-ahead baseload power fell by 26.3% to average £48.9/MWh in December, the first monthly loss since August. On Friday 23 December, the contract reached £44.0/MWh, an 11-week low, with low demand levels over the Christmas holiday period

- The-month ahead contract dropped 31.2% to £54.1/MWh

Key Market Drivers

- There was little influence from the French power market, which has driven the UK market in recent months.

The IFA interconnector with France is on an extended outage, with capacity down 1GW between November 2016 and February 2017. This has reduced exports and helped to stabilise prices during French supply concerns. - EDF restarted two of its French nuclear reactors during the month; however, three others had outages extended into early January.

*£ per MWh (Annual forward average)

European Gas

- European gas prices all increased in December.

- GB prices ended the month 1.8% higher than Belgian prices, 15.7% higher than German prices and 7.9% above Dutch prices.

- European gas and power prices were supported by OPEC’s historic agreement from the meeting held on 30 November. At the meeting, OPEC agreed on its first oil output reduction since 2008, in a move to support oil prices.

- In early December, Norwegian flows improved as outages ended. However, new unscheduled outages were then reported at Norway’s Kollsnes gas processing plant and at the Gullfaks and Troll fields.

- Additionally, outages were reported at Holland’s largest storage site, Bergermeer, pushing up Dutch prices and reducing interconnector exports to the UK.

- UK import volumes through the Belgium-UK and Holland-UK interconnectors reportedly reached three-year highs at the beginning of December. However, these levels reduced by around two thirds later in the month.

European Power

- European power prices experienced mixed movements in December.

- GB prices ended the month 6.2% above French prices, 44.7% higher than German prices and 43.0% above Dutch prices.

- French nuclear output concerns were reduced following the restart of two reactors, even though three others had outages extended into early January.

The UK-France power interconnector was damaged on 21 November. National Grid confirmed at the end of November that half of the link’s 2GW capacity will be out of action until the end of February. - German nuclear outages will stretch deeper into January after RWE and EnBW delayed the planned return dates of two reactors for additional maintenance.

World Oil

- Brent crude oil prices rose 16.2% to average $54.9/bl in December, with prices above the $50.0/bl mark for the entire month. Prices went up throughout the month, reaching $57.0/bl on 30 December – the highest price since July 2015. Prices were largely supported by OPEC’s historic agreement from the meeting held on 30 November. At the meeting, OPEC agreed on its first oil output reduction since 2008. The deal also included the group’s first coordinated action with non-OPEC member Russia in 15 years.

Coal

- API 2 coal went down 6.4% to average $65.8/t in December, with Colombian coal workers calling off a planned strike. The fall came despite strong physical demand in China. On 8 December, prices reached an 11-week low of $59.2/t.

Carbon (EU ETS)

- EU ETS carbon lost 8.0% to average €5.2/t. On 5 December, prices fell to an 11-week low of €4.2/t.