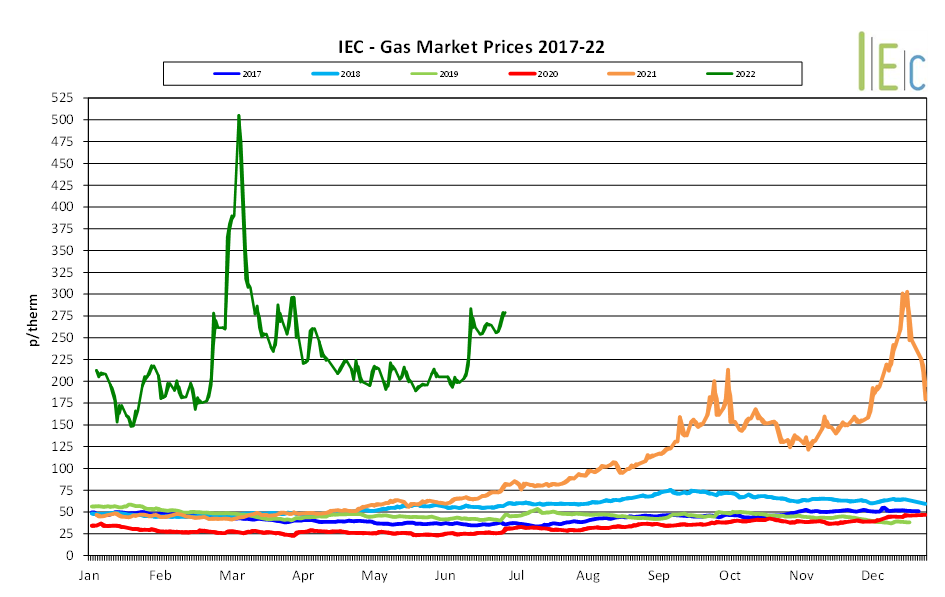

Following a settled spring, the market bounced mid-June following news breaking of a fire at a US LNG Terminal in Freeport, Texas and growing reports of the potential supply disruption which may occur during the approaching period of Nord Stream 1’s maintenance.

Anxiety around European supply continues to be the main driver behind the global gas markets. Regular geopolitical statements around import/export sanctions between the EU and Russia continue to be briefed, while daily fluctuations in Russian gas flow onto the continent have the markets on high alert.

The summer maintenance period is approaching, adding further pressure to the markets with the major concern surrounding Russia’s Nord Stream 1 which transports gas towards Germany.

Flows have fallen to around 40% capacity by end of June, and there are long-term fears for Q422 supply should capacity not increase following its maintenance period starting 10th July.

These fears have led Germany to announce it has entered Phase 2 of its emergency gas contingency plans – increasing credit lines to fill gas storage and encouraging industrial users to save on gas.

European storage capacity has finally reached its 5-year average level, hitting 58% full by the end of June. The UK’s own storage capacity, despite a few unplanned withdraws which were required to help balance its system, levels remain significantly higher than the 5-year average 95% vs 41%.

Although the UK gas system experienced intervals of short supply across June, with reduced imports from Norway as they actioned their own planned and unplanned maintenance procedures, the strong storage capacity built up earlier in the year helped to avoid any major issues. Long spells of low wind strength also increased gas demand for power generation, however, these were eased by temperatures remaining around seasonal norms. LNG deliveries continue to arrive, though now at a steady pace rather than the flood seen earlier in the year, with the price premium now swinging towards the Asian market.

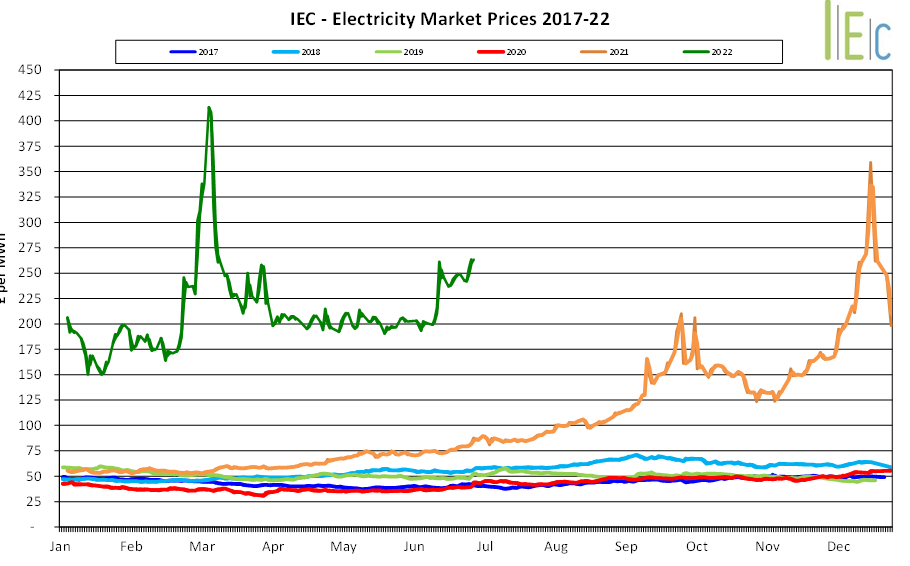

Electricity

Volatility in the gas markets continues to govern the electricity prices, with a significant rise taking place in the middle of June and sustaining for the remainder of the month.

Despite no major UK system issues, periods of low wind strength continue to limit renewable capacity available – average renewable generation was 24%, in turn strengthening its dependence on gas for power generation and the exposures of its market.

Carbon prices remain high due to many EU countries reverting back to coal-burning for power generation, however, the EU has bowed to pressure and granted additional carbon certificates in an attempt to aid demand and curb the price. EUTS and UKTS prices ended the month a €83.35 and £84.40 per tonne, respectively.

Processing...

Thank you!Your subscription has been confirmed.You'll hear from us soon.