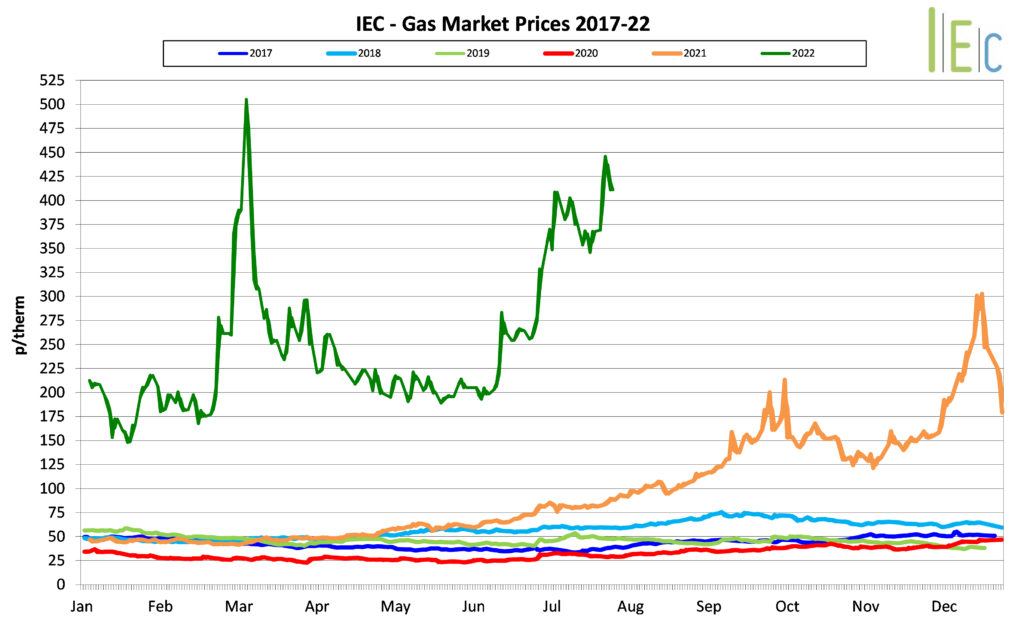

The month started bullishly with news that the fire damage caused at the Texas LNG Terminal was more severe than originally thought, meaning full operations may not resume until the end of the year. Additionally, threats of an impending strike from Norwegian gas workers which would reduce flows down to 55%, these reports sent both short- and long-term prices soaring.

Although the gas worker’s strike threats were short lived with the Norwegian government averting the action by stating it would be illegal due to its wider effects on European supply, prices remained supported due to a string of unplanned outages affecting flows from Norway and mainland Europe. There was also increasing anxiety around the approaching maintenance period for Russia’s Nord Stream 1 with uncertainty around both how long it would be offline and whether future gas flows would remain at 40%, increase or even decrease.

These fears were realised on 26th July, after a few days of flows returning at 40% capacity, they were reduced to 20% and have not increased since. This again sent prices rocketing up to highs which have not been seen since the early days of Russia’s invasion of Ukraine.

Current European gas storage levels are in line with 5-year average at 69%, though gas flows into Europe now down to record lows, it will be a race against time to replenish their storage levels before the winter season begins in October.

The UK gas system has continued to experience intervals of short supply, with reduced imports from Norway from both planned and unplanned maintenance procedures, as well having issues along the UKCS interconnector with Belgium. There has also been increasing demand on gas for power generation with a mid-month heatwave sending temperatures it new record highs and periods of high pressure reducing wind strength. Despite these pressures, storage levels have been boosted up to 100% capacity by the end of July. LNG deliveries continue to arrive, though now at a steady pace rather than the flood seen earlier in the year, with the price premium now swinging towards the Asian market.

Electricity

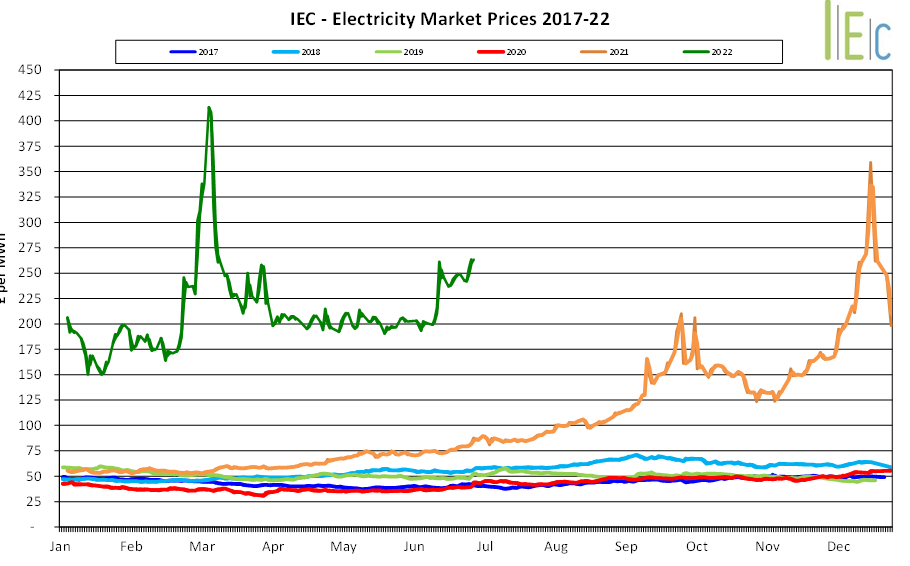

The volatility in the gas markets continue to have a major influence on the electricity prices, however the situation has been exacerbated further due to the peak demand requirements of the summer season and the rising temperatures that have been recorded across Europe.

There has also been additional pressures on the European markets due to France’s Nuclear fleet requiring additional maintenance and extended periods offline.

The UK electricity system continues to be heavily reliant on gas for power generation with periods reaching up to 69% of the generation mix, as during periods of low wind strength limit renewable generation and Nuclear consistently providing 20%.

Thanks to the EU bowing to industrial pressures and granting additional carbon certificates, the demand curbed allowing prices to settled throughout July, though this provided little aid to the power prices. EUTS and UKTS prices ended the month at €78.35 and £78.50 per tonne, respectively.

Processing...

Thank you!Your subscription has been confirmed.You'll hear from us soon.