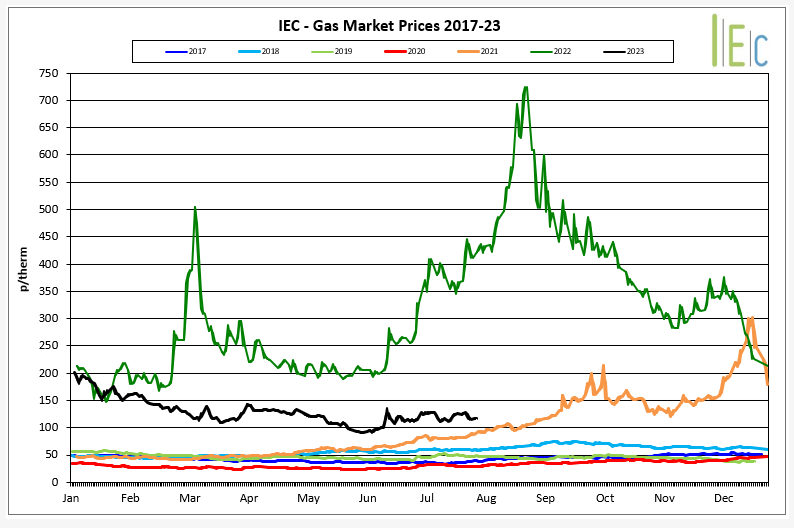

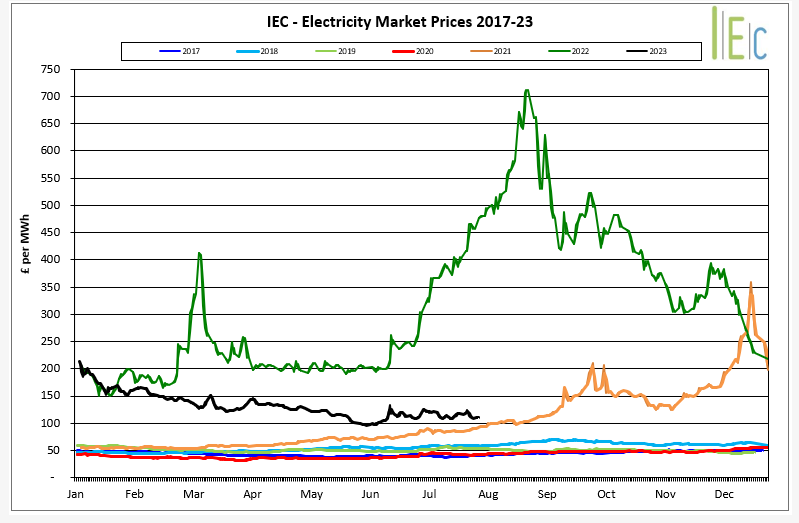

Following a significant maintenance period experienced throughout June and July, Norwegian gas flows notably increased at the end of July.

This was partly in response to the extended maintenance at the Nyhamna gas plant ending on the 15th July, although further maintenance is scheduled in August which could result in additional price volatility.

UK and European gas storage levels remained strong at 80% and 85% respectively at the end of the period. Storage levels are still anticipated to be full by mid-September if the current injection rates continue. However, there are still some concerns that a cold snap or more supply disruption in the coming weeks could impact Winter 2023 pricing.

As was experienced in June, a reduced number of LNG cargoes arrived on the UK and European shores in July. Supply has been impacted by continued maintenance at a number of US terminals but also increased demand from the Asian market. Warmer weather in this part of the world has resulted in Asia being more competitive on LNG prices which has consequently reduced the number of ships arriving in the UK and Europe. These reductions in LNG cargoes have created some hesitancy in markets with gas storage levels not at capacity as yet.

Renewable generation has been inconsistent throughout the month with reduced wind generation putting further pressure on gas for power generation. Strong PV generation in Southern Europe has countered an increase in electricity demand across the region which has been created by the extreme recent temperatures they have been experiencing. July also saw some reduction in French nuclear capacity, although this had a minimal impact on pricing. This volatility around supply though has led to an increased number of customers hedging their Winter 2023 position in recent weeks.

Russia have reiterated their stance that it will retaliate if they find any evidence of deliberate sabotage to Nord Stream 1. Consequently, markets remain cautious about further disruption but have adapted to the ongoing Russian conflict with Ukraine. Russian pipeline gas flows to Europe hit a seven-month high in July, primarily driven by record deliveries through the European string of the TurkStream pipeline. At present Russian pipeline gas is currently limited to flows via Ukraine entering at the Sudzha point on the Russia-Ukraine border and through the European string of TurkStream.

Brent crude oil prices rallied above $84/bbl by the end of July. Prices are supported as reports indicate that Saudi Arabia intends to extend its supply cuts into September, which were initially anticipated to end to during August. With Saudi Arabia being the world’s largest oil exporter, these expected cuts are only likely to tighten global supply further. Strong economic activity in the US and India has led to experts revising their global oil demand forecasts which have sustained pricing further.