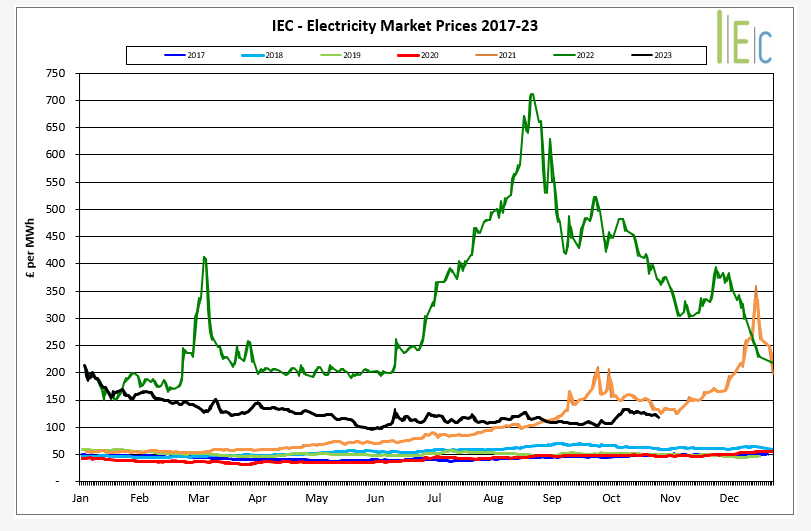

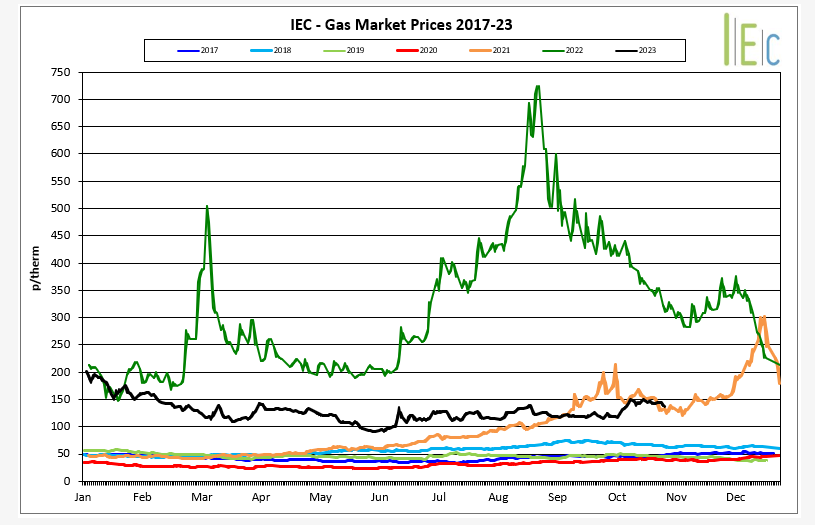

October saw a significant level of price volatility, primarily stemming from the emerging conflict in the Middle East.

Market sentiment was bearish at the beginning of the month with temperatures above seasonal norms and strong supply and storage fundamentals.

However, the kidnapping of over 200 hundred Israeli hostages by the Gaza based terrorist group Hamas on the 7th October, and the subsequent military action by Israel, resulted in bullishness across the curve.

This was heightened further when production at the Israeli gas field at Tamar was suspended shortly after, and then later in the month when Israel began their ground assault on the Palestinian territory.

Gas storage in the EU and UK has remained at record high levels, with EU storage sitting at 99% at the end of the period. Norwegian gas flows were very strong by the end of the month as a result of various maintenance work being completed across October. There were concerns during the month that damage to a gas pipeline between Finland and Estonia could be the result of sabotage which stoked further security of supply fears (following the explosions of a Nord Stream pipeline in the Baltic Sea last year). Although the incident in Finland was later confirmed to have been damaged by the anchor of a passing ship. Temperature forecasts for November and early December suggest a milder direction, which adds to the general bearish market pressure seen at the end of October. Although this could quickly alleviate if there are further escalations in the Middle East or Ukrainian conflicts.

There are concerns that hostilities in the Middle East may reduce LNG supply as several countries in the region are key exporters and if they were to become entangled in the dispute this could affect global LNG supply lines. Any potential shipping restrictions in the Suez Canal could also influence LNG supply to the UK with Qatar being a major supplier who could be impacted. Tensions remained at the Chevron operated LNG Facilities in Australia as unions accused operators of renegading on a previous agreement. This led to the mid-month announcement that further strike actions would take place before a resolution was swiftly agreed to prevent any industrial action.

It was recently announced by the Imperial College London that in June 2023, Great Britain’s installed wind capacity surpassed gas generation capacity for the first time. The installed wind capacity registered 27.9GW compared to 27.7GW for gas. This is a notable milestone for future decarbonisation for the UK. National Grid has announced an initiative to fast-track the connection of up to 20GW of clean energy projects to its electricity transmission and distribution networks. This plan will increase the capacity of renewable energy sources within the grid across England & Wales. National Grid intends to offer new connection dates to 19 battery energy storage projects on its transmission network, with a total capacity of 10GW, with the hope that they will be able to connect four years earlier than initially agreed.

In October Saudi Arabia and Russia confirmed they would continue with their additional voluntary oil output cuts until the end of the year due to concerns over demand and economic growth. OPEC however have forecasted strong growth in global oil demand in 2024, due to an anticipated increase in Chinese demand next year and their belief the current resilient world economy will continue. The end of the period saw Oil prices fall to around $87/bbl as the rising output from OPEC and the United States had a greater influence on markets than the ongoing troubles in Israel and Gaza.