Norwegian gas maintenance interrupted supplies in August and this persisted into early September which led to some concerns around capacity for the upcoming Winter.

The period saw reduced gas flows across as the Troll gas plant experienced several outages, however the plant was back to full capacity by the end of the month. Unscheduled outages at a number of other facilities have also effected Norwegian exports across the period.

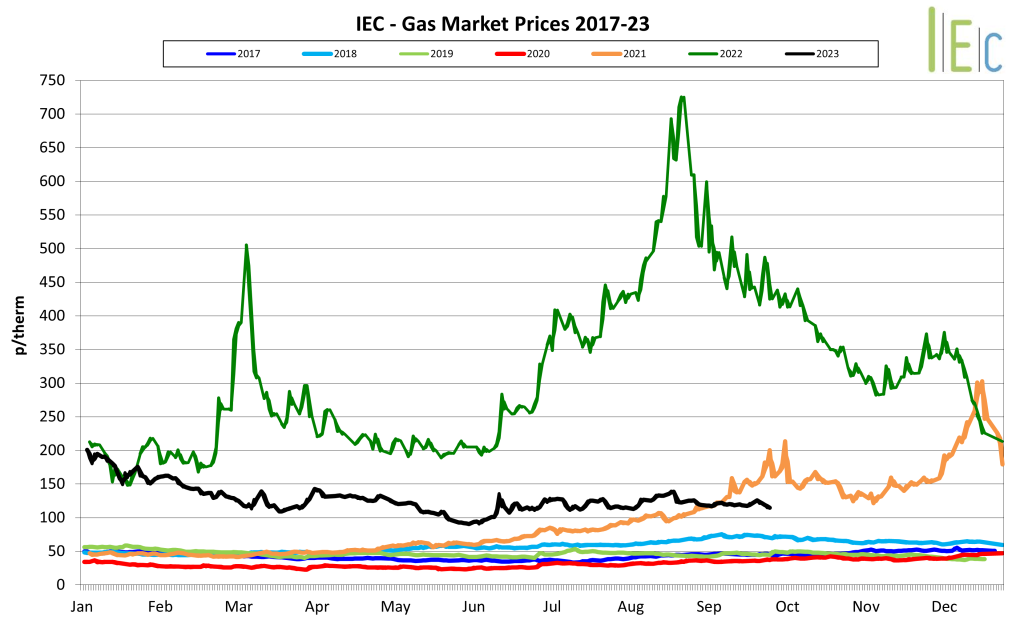

European temperatures for September remained above seasonal norms and this was expected to continue into early October. This created some bearish sentiment within markets which was further increased by EU Storage Levels sitting at 95% by the end of the month. This is significantly above the November 90% target set by The European Commission and the 5-year average of 87%. UK gas storage depleted to 64% by the end of September. UK Gas storage is inadequate with there only being enough capacity to supply 12 average days (or 7.5 days during winter peaks). This is compared to average gas storage of 108 days in Germany and 126 days in France. The low storage capacity emphasises the importance the UK holds on UKCS and Norwegian gas flows, as well as regular LNG arriving onshore.

Regarding LNG, the month began with the two Chevron-operated LNG facilities in Western Australia beginning partial industrial action. However, the threat of full strikes dissipated as an agreement was made prior to a scheduled tribunal towards the end of the month. LNG deliveries into the UK throughout September remained low and at a similar level to previous months. These are expected to increase in October with a dozen cargoes already confirmed and more anticipated.

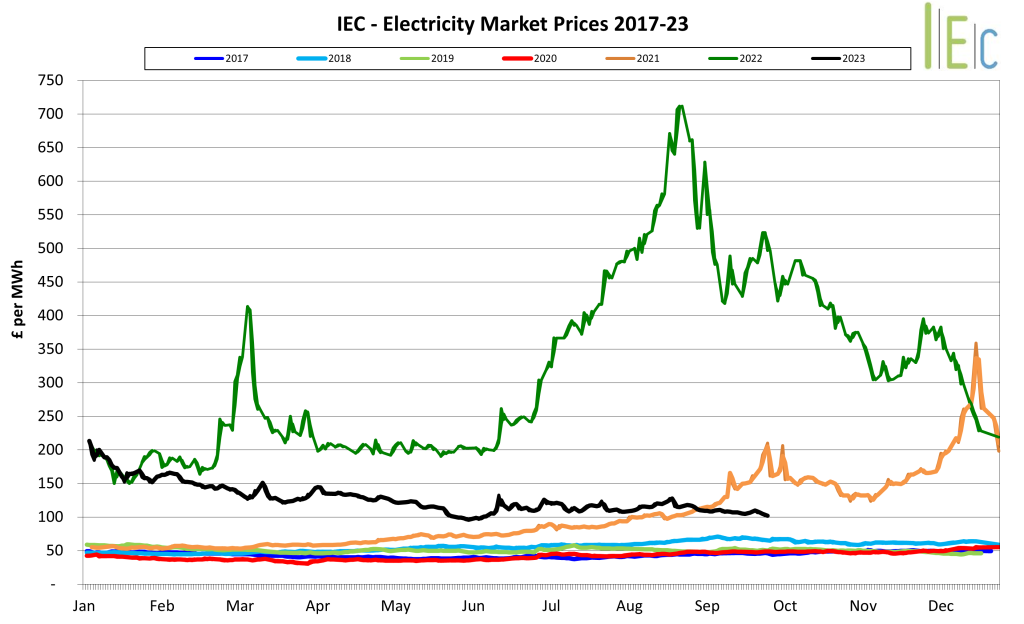

Wind generation has been extremely healthy in the UK and Europe across the period, with Storm Agnes creating high wind speeds across the UK to boost the generation yield. The UK imports electricity via multiple interconnectors with the majority being exported from French nuclear facilities. Therefore, with the French nuclear output continuing to look more stable and available (especially when compared to Winter 2022) this is a positive that should put downward pressure on prices. A new interconnector from Lincolnshire to Denmark is due to come online in January 2024. This should provide access to a potential 1.4 GW supply of power to the UK and will be a significant benefit to the grid during the peak winter months.

Brent crude oil prices rallied to over $90/bbl in September as OPEC’s top producer and the largest crude oil exporter in the world, Saudi Arabia, has extended its extra 1 million barrels per day cut from the end of September until the end of this year. US inventories have also depleted over the last two months to offer further support to oil prices. The expectation is that prices will remain boosted if supply is tighter and demand increases from recovering economies (such as China) over the coming months.