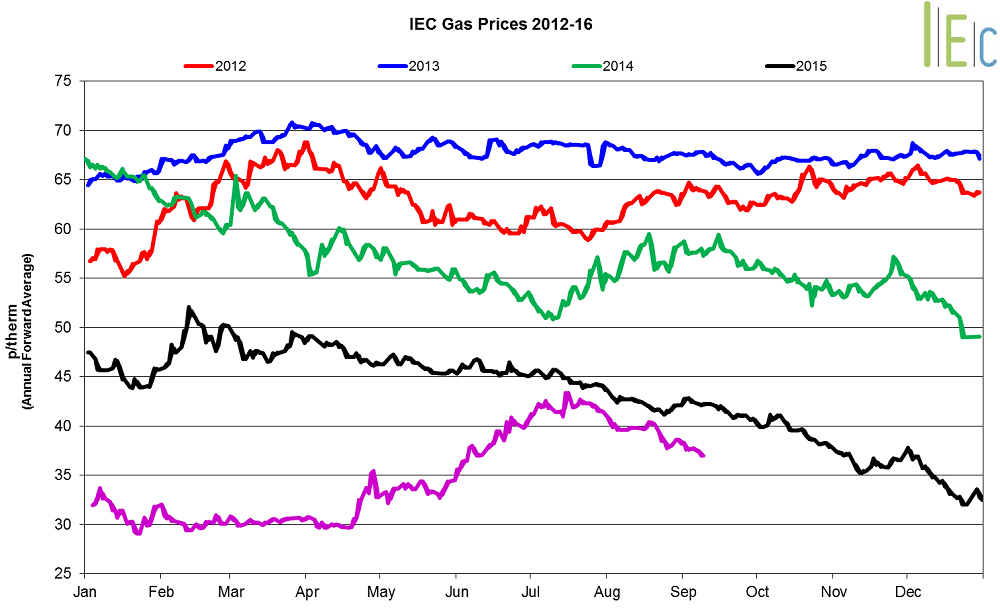

Gas market trends

What’s been happening?

- All seasonal gas prices decreased in August. The annual October 16 gas contract lost 6.0% to 40.0p/th. Winter 16 gas experienced the largest drop, at 6.1%, to average 42.0p/th. Summer 17 gas decreased 5.8% to 38.0p/th.

- Day-ahead gas moved 10.2% lower to average 31.1p/th. On 31 August the contract reached its lowest price in over six years of 26.0p/th.

Key market drivers

Centrica announced that it will make 20 wells available at Rough gas storage facility from 1 November 2016. This has improved the supply outlook for the coming winter and pulled the winter 16 price down to reach a two-and-a-half-month low of 39.8p/th on 31 August.

* £ per p/therm (Annual Forward Average)

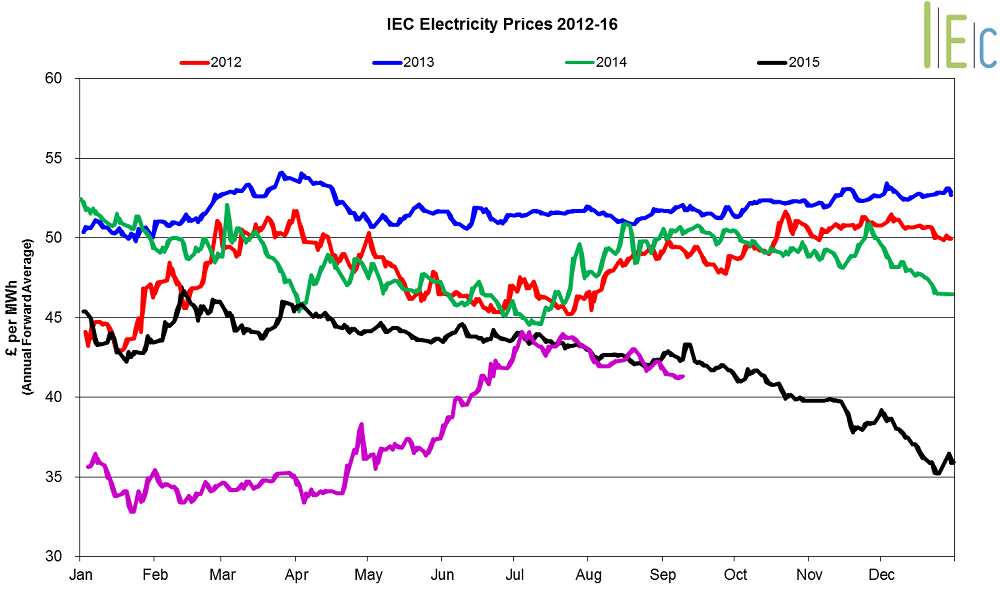

Power Market Trends

What’s been happening?

- The annual October 16 baseload power contract fell 3.0% to average £42.4/MWh, following the gas market lower.

- The day-ahead contract started the month at a six-month high of £42.0/MWh before decreasing as the month progressed to £33.1/MWh on 31 August. The month-ahead contract dropped 5.6% to average £37.6/MWh during August.

Key market drivers

- The winter 16 power contract lost 2.8% to average £45.8/MWh. The contract followed its gas counterpart lower, which dropped on news that Rough gas storage facility would have some available capacity for the coming winter. Summer 17 decreased 3.2% to £39.0/MWh.

*£ per MWh (Annual forward average)

European Markets

- All European gas prices decreased in August. GB gas prices ended the month 1.3% below Belgian prices, 6.9% lower than German prices and 3.4% below Dutch prices. Prices were pushed down by high UK exports and lower oil prices.

- European power prices were mixed in August. French prices experienced the largest overall gain, up £4.2/MWh to £33.5/MWh. GB prices ended the month 4.1% below the continental European average of £29.1/MWh.

Commodity markets

- Brent crude oil prices lost 0.2% to average $46.7/bl in August. Prices have fallen from their near eight-month high of $52.2/ bl in June. This was caused by continuing concerns of oversupply in the market and uncertainty in global markets.

- API 2 coal lost 1.3% to average $58.3/t. Prices fell on the back of lower European demand levels. In the UK specifically, coal-fired power generation in Q216 hit a record low.

- EU ETS carbon gained 1.7% to average €4.7/t. On 2 August the price of EU ETS carbon fell to €4.4/t, the lowest price since March 2014.