Despite Europe’s ongoing storage and supply issues over the past few months, UK gas storage has now reached average levels for this time of year after facing significant reduction for many months.

Nevertheless, prices remain high, supported by poor supplies into Europe of both piped gas and LNG. The lack of piped gas supply is being caused by ongoing issues with Norway’s supply coupled with low Russian flows which have continued to force withdrawals during the summer months, a time when we would normally expect injections.

LNG tankers continue to head east, limiting arrivals to European hubs. This, coupled with the impact of Hurricane Ida has meant supply chains are experiencing serious delays in replenishing their storage levels.

The accumulation of these global supply and storage factors has resulted in concerns for winter 2021-22. Therefore, as we approach the colder months, prices are likely to continue rising unless supply improves.

A strange price dip was reported on August 20th due to an error in the gas pricing algorithm, which wrongly assumed that Nord Stream 2 had started delivering gas. This was swiftly rectified and the price rebounded within a day. However, this dip does present a level of optimism that once the Nord Stream 2 pipeline is fully operational, prices should start to ease.

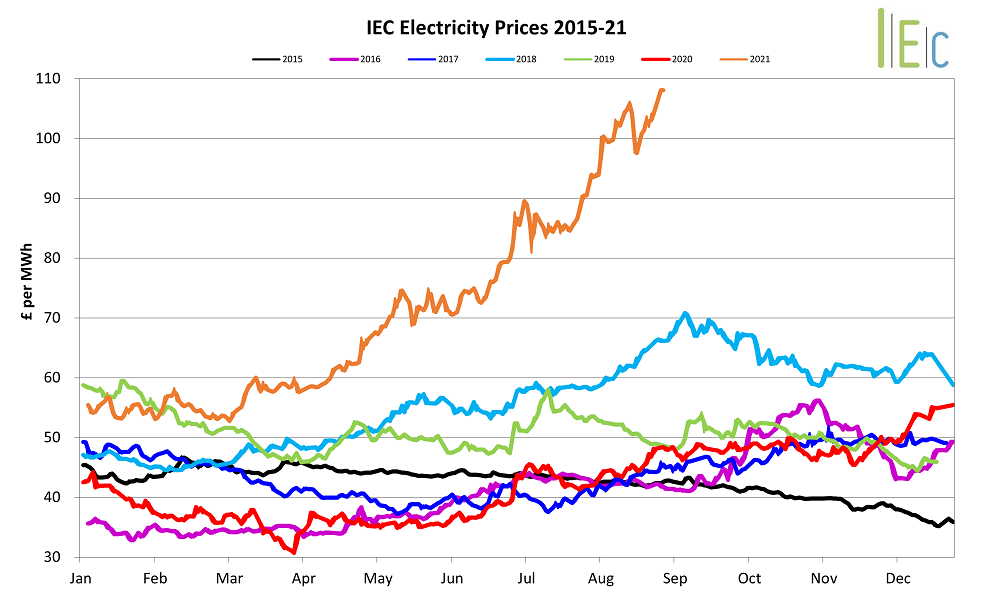

Electricity

The UK electricity market continues to mirror gas trends, also reaching new highs at the end of August. On average, gas was utilised for around 50% of the UK’s average fuel mix for electricity throughout August.

Low wind also continues to hinder the renewable capacity, causing a higher reliance on gas and nuclear power, adding to the rising power prices.

The UK’s carbon markets have been relatively stable throughout August despite the European market reaching new records of €61.01 per tonne.

Oil

Brent Oil prices presented a slight dip towards the end of August as a result of Hurricane Ida, closing at 72.61 USD per barrel, but have since begun to rise again, displaying prices similar to July’s 75 USD per barrel.

Some analysts predict further price rises amid tightening crude supplies and increasing demand over the coming months as OPEC+ stick to their plan of adding 400,000 barrels per day to the market.

Coal

A British Gas spokesman has announced that relying on coal to replenish gas shortages is not an option “given the high carbon price and the phaseout of coal generation in the UK”.

Meanwhile, the last three coal-fired power plants in the UK, owned by Drax, EDF, and Uniper announce plans to cease generating coal by September 2024.

Processing...

Thank you!Your subscription has been confirmed.You'll hear from us soon.